Welcome to Tenancies-in-Common (TIC) Week on the SLCG Blog

Oct 2013

Today, SLCG posted a new research paper, Large Sample Valuations of Tenancies in Common . In it, we value 194 TICs, totaling $2.2 billion in equity and representing approximately 17% of the TIC industry from 2004 to 2009. Our paper complements our earlier research on TICs ("What is a TIC Worth?" and "Private Placement Real Estate Valuation"), and is the most extensive empirical study of TICs to date. This week we will be summarizing the results of our research in a series of blog posts. But to start, let's address some basic questions about TICs.

What are TICs?

TICs are real estate investments owned jointly by two or more entities. The real estate is undivided, meaning that no particular tract of the land or building on the land can be identified as belonging to a particular entity. While TICs can result from family gifting when a property is inherited by multiple family members, for example, our focus is on syndicated TICs sold to retail investors. Syndicated TICs are private placement real estate investments that are packaged and sold by professional real estate sponsors.

The vast majority of TICs purchase an income-generating property with the proceeds from an equity issuance and a mortgage loan. TICs anticipate holding the property for a period of several years (typically 7-10 years), throughout which they pay monthly distributions to TIC investors as well as any interest and principal due on the loan. TICs are designed to sell their property and distribute the sales proceeds to investors after paying the outstanding mortgage balance and sales fees.

Why did real estate investors purchase TICs?

TICs were sold as a way to defer capital gains taxes on the sale of real estate property. Capital gains taxes are typically due at the time of the sale of a business or investment property if the sale produces a gain. However, Internal Revenue Code's rule 1031 allows the payment of taxes to be postponed if the sales proceeds are used to purchase similar property or what is known as a "like-kind exchange." TIC issuance increased dramatically after 2002, when the IRS adopted Rev. Proc. 2002-22 (PDF) "clarifying when acquisition of a tenant-in-common interest in real estate qualifies as replacement real estate under Section 1031."

How much TIC equity was sold over the years?

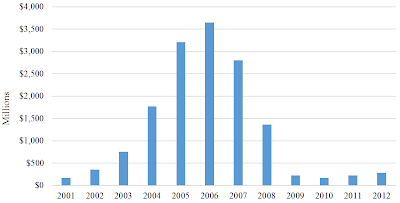

The total amount of equity invested in TICs increased from $167 million in 2001 to $3.7 billion in 2006. After 2007, many TICs stopped paying distributions to equity investors. It was not uncommon for non-performing TICs to undergo loan refinancing that effectively wiped out the value of the equity interests. The industry shrank precipitously from 2007 to 2009 and, with $278 million issued in 2012, is currently a small fraction of what it used to be. The following figure shows the equity invested in TICs from 2001 to 2012.

Equity Invested in TICs

What are some of the problems with TICs?

TICs charge investors high upfront fees on the order of 15% to 30% of gross offering proceeds, often more than offsetting the benefit of capital gains tax-deferral. In addition, TIC offering documents are often misleading and incomplete. Their financial projections compute "cash-on-cash" return rates that often include repayment of contributed capital held in reserves in what appears to be income. TIC sponsors often use aggressive assumptions in their cash flow projections that mislead investors into expecting higher than reasonable returns.