Investors in Residential Mortgage Backed Securities (RMBS) have suffered tremendous losses since 2007. Many junior and mezzanine investors were wiped out by the asset pools' delinquency rates coupled with the subordination embedded in these structured securities. Since then, there has been a proliferation of litigation alleging that the underwriters and originators of RMBS misrepresented the risks of these products. An interesting new paper by Professors Piskorski and Witkin of Columbia Business School and Professor Seru of the University of Chicago, take a close look at misrepresentations in a dataset of 1.9 million loans originated from 2005 to 2007. Their research merges loan-level data on privately securitized mortgages (non-agency RMBS) and borrower-level credit report data and find that "buyers [of non-Agency RMBS] received false information about the true quality of assets in contractual disclosure by intermediaries during the sale of mortgages."

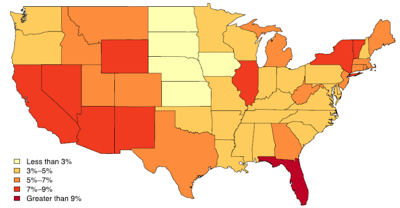

The paper concentrates on two types of misrepresentations: 1) whether a loan reports the occupancy status of the borrower correctly--whether the home is used as a primary residence--and 2) whether a loan reports to have no simultaneous second liens when it does in fact have a second lien. The authors find that about 9% of all loans examined include one or both misrepresentations. The authors also find that the fraction of loans misrepresented was larger in states with higher pre-crisis growth in home prices, such as Arizona, Florida, California, and Nevada.

Fractions of Loans Reported As Owner-Occupied that Misreport Occupancy Status

Source: Piskorski, Seru, and Witkin (2013)

The authors also find that misrepresentation of collateral along these two dimensions significantly increases the risk of default. What's even more interesting is that their paper finds evidence that the higher default risk of misrepresented loans was, at least in part, priced into the loans by the lenders. Loans with misrepresentations were charged a higher interest rate, suggesting that lenders were aware of these loans' higher risks.

Although it seems like lenders incorporated knowledge of the true quality of the loans into their pricing by charging a higher interest rate on loans with misrepresentations compared to otherwise similar loans, the authors find no evidence that knowledge of the misrepresentations was reflected in the prices RMBS investors paid for the securities. They examine the average yield spread to Treasury securities and the level of subordination protection for the senior tranches in a sample of 353 mortgage pools finding "little evidence that misrepresentations were reflected in the initial prices of the RMBS securities."

The paper documents some of the pitfalls of modern mortgage financing and securitization though clever use of exclusive datasets The packaging and reselling of mortgage pools allows the true quality of the assets in the pool to be misrepresented making it impossible for investors to assess their risks. The authors extrapolate to the pre-crisis $2 trillion non-agency RMBS market, and estimate that enforcement of the representations made to investors would lead to repurchases at par of about $160 billion (8% of the market) in loans by mortgage originators and underwriters. Given that their analysis only spans two criteria--owner occupancy and second liens on loans--their paper is likely to report a conservative lower bound for the prevalence of misrepresentations in non-agency RMBS loans.