State Pension Funds Would Benefit from Passive Indexing

Jul 2013

The Maryland Public Policy Institute and the Maryland Tax Education Foundation released a report that uses data on state pension funds to question the value of active money management. The report finds that paying Wall Street managers to actively select and trade securities in state pension funds does not generate better investment returns, although it does provide higher fees and commissions for Wall Street managers. The results are in line with that of the S&P Indices Versus Active Funds (SPIVA) Scorecard that we covered earlier this year that found that most active managers underperformed their benchmark indexes during 2012.

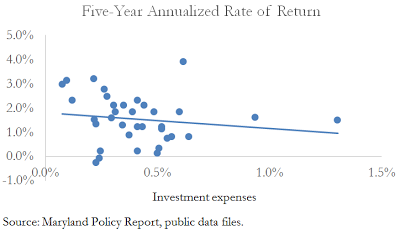

The Figure shows the five-year annualized rate of return and the investment expenses as a fraction of net assets for 35 states with a fiscal year-end of June 30. Focusing on this set of states allows the comparison of the annualized rate of return for the same time period. Each dot on the Figure represents a different state and the solid line on the Figure is the trendline. The trendline's slightly negative slope shows that higher investment expenses are typically accompanied by slightly lower rates of return on investment.

According to the report's public data files, South Carolina was the state with highest investment expense with annual fees that equaled 1.31% of beginning-of-year net assets. The median investment expense of all 46 states reviewed was 0.39%. The authors state that indexing fees would equal about 0.03% annually and thus conclude that by indexing most of their portfolios, "the 46 state funds surveyed could save $6 billion in fees annually, while obtaining similar (or better) returns to those of active managers."

The Maryland think tank argues that state pension funds should consider passive indexing. Such a switch from active management to passive management would be in line with current investment trends. Although active management funds still represent about 72% of the market, they made up 86% of the market a decade ago according to this article. In fact, the California Public Employees' Retirement System, with $1.64 billion in defined-contributions plans, has recently voted to replace all actively managed funds with passive options citing cost savings as the main reason for their switch. It remains to be seen whether other states will follow suit.