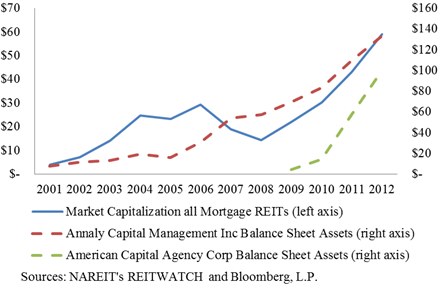

Instead of investing in real estate property directly like equity real estate investment trusts (REITs) do, mortgage REITs borrow in the repo markets and invest in mortgage backed securities (MBS) -- mostly residential MBS issued by Fannie Mae, Freddie Mac, and Ginnie Mae. The current environment of low interest rates has kept the borrowing costs low for mortgage REITs, facilitating their outstanding growth. The figure shows the market capitalization for all listed mortgage REITs and the total assets for the two largest players in the industry: Annaly Capital Management (NLY) and American Capital Agency Corporation (AGNC).

Even though their business model experienced setbacks during the financial crisis (due to lack of funding for short-term borrowing), the market capitalization of all mortgage REITs has increased by almost 15-fold in the last twelve years. Their growth accelerated from 2008 onward, when the Federal Reserve's policies drove borrowing rates to record lows.

Retail investors can directly purchase mortgage REITs through their brokerage accounts. What they may not know is that mortgage REITs are not regulated investment companies and hence do not afford investors the benefits of the Investment Company Act . Many open-end and closed-end investment companies invest in agency MBS, just like mortgage REITs, but must comply with leverage limits established in the Investment Company Act. For example, closed-end companies may only borrow up to 33% of their assets. By contrast, the average debt-to-asset ratio of listed mortgage REITs is over 84% according to REITWatch. This higher leverage can enhance returns when the market is doing well but it also poses a higher risk of losses in the event of a downturn.

The added risk caused by the leverage embedded in mortgage REITs is one of the reasons behind a 2011 inquiry by the Securities and Exchange Commission (SEC) into the mortgage REIT business. In the SEC's concept release and request for comments, the SEC states that "certain types of mortgage-related pools today appear to resemble in many respects investment companies such as closed-end funds and may not be the kinds of companies that were intended to be excluded from regulation under the Act." It is likely that the sector's outstanding growth and increasing risks will attract further attention from the regulators.

Another issue that investors should consider is the management capabilities of some of the mortgage REITs. A negative consequence of the high growth in the sector is that REITs that started out as relatively small players and have benefited from outstanding growth may currently have an asset portfolio that exceeds their management capabilities. Armour Residential REIT Inc. (ARR), whose assets have ballooned from $250 million at the end of 2008 to over $20 billion at the end of 2012, has been described as an example of a mortgage REIT whose management may have difficulty keeping up with the risks of its growing balance sheet.

As the economy shows signs of recovery, it seems likely that the Federal Reserve's policy will shift in the near future. A rise in the short-term interest rates will directly affect the profitability of the mortgage REIT industry, by reducing the wedge between the interests earned on its long-term investments and its short-term borrowing costs. In addition, a large-scale sale of MBS by the Federal Reserve could depress the prices of MBS and negatively affect the price of the portfolio holdings of mortgage REITs.* The high leverage typical of the industry may exacerbate these risks. We will continue to monitor mortgage REITs and their rising risks.

_______________________________________

* The Federal Reserve has amassed about $1 trillion in agency mortgage backed securities. For the Federal Reserve's balance sheet, see the Federal Reserve Board's flow of fundsreport .