Higher Expected Returns Only Come from Higher Risk: The Case of 130/30 Strategies

May 2013

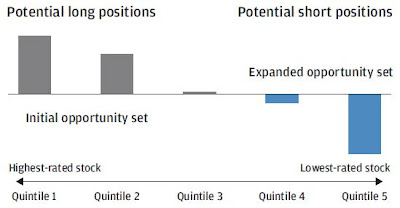

JP Morgan recently released an "Investment Insight" that puts the spotlight on 130/30 strategies, which are used by several mutual funds and ETFs from a variety of issuers. A 130/30 strategy involves selling short 30% of the assets in a portfolio and using the proceeds to leverage the long securities to 130% of initial assets. The securities that are shorted are expected by the portfolio manager to depreciate during the holding period (overvalued) while the assets that are purchased are expected to appreciate in value during the holding period (undervalued). The report offered the following illustration of the strategy:

Source: JP Morgan

The JP Morgan report also notes that 130/30 strategies can increase returns while keeping the portfolio's beta--its relationship to the broader market--the same as a long-only portfolio. However, this does not mean that 130/30 strategies achieve riskless profits. Shorting securities involves a number of additional risks (including the potential for > 100% losses), even for large cap, highly liquid stocks. In addition, the 130/30 ratio is not fixed for all funds -- shorting is limited to 50% of assets by the leverage limits imposed by the Federal Reserve Board's Regulation T.

But perhaps the most important risk of 130/30 strategies is that they depend on the manager's ability to pick overvalued assets and undervalued assets. We've seen evidence, including recently updated evidence, that managers are not great at picking stocks within a given fund to beat a benchmark. Furthermore, there is evidence that managers often do no better than chance when outperforming their peers. In other words, if you're looking for a manager who will outperform half of their category peers, you are no better off looking at past performance than you are by flipping a coin.

Given this evidence, how much trust do you want to put into a fund that leverages their exposure to the manager's (or some proprietary algorithm's) stock picking ability? In 2009, a report on 130/30 funds found that their performance was severely lacking, and many 130/30 funds closed shortly after the financial collapse. That report, titled "130% Gimmick/30% Good Idea", included sweeping criticisms of the fundamentals of this strategy, especially that it is almost entirely dependent on hard-to-identify manager skill.

A fundamental concept of finance is the fact that higher expected returns only come at the cost of additional risk. Although JP Morgan states that there is no additional "market risk", there is additional risk and investors should not think that such strategies are a free lunch. As usual, investors should also be conscious of fees. Fees for these funds can be high and higher fees have a significant detrimental effect on realized investor returns.