Feb 2013

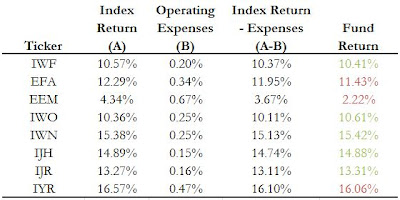

Securities lending plays a big role in the performance of ETFs. In a logical world, ETF investors should expect to get the returns of an index minus the expense ratio.

Earnings from securities lending allow many larger ETFs to outperform their expense ratio, though, according to Mike Rawson, ETF analyst at Morningstar Inc.