SEC Charges Morgan Keegan Directors with Failing to Oversee Asset Valuations

Dec 2012

The SEC has charged eight former Morgan Keegan directors with failing to provide accurate valuations for mortgage-backed securities during the subprime crisis of 2007. We wrote a paper in 2009 explaining the collapse of the RMK bond funds and how they relate to these very same securities.

The mutual funds at issue are 1) RMK High Income Fund, Inc.; 2) RMK Multi-Sector High Income Fund, Inc.; 3) RMK Strategic Income Fund, Inc.; 4) RMK Advantage Income Fund, Inc.; and 5) Morgan Keegan Select Fund, Inc. The Select Fund was an open-end company which contained three open-end series-the Select High Income portfolio, the Select Intermediate Bond portfolio, and the Select Short Term Bond portfolio.

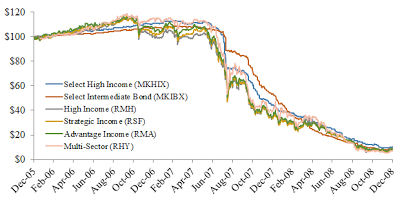

The RMK funds were essentially the same fund. They behaved in the same manner and held many similar securities. Below is a graph of the return if someone invested $100 on December 31, 2005 with reinvested dividends. By December 2008 an investor would have loss about 90% of the investment.

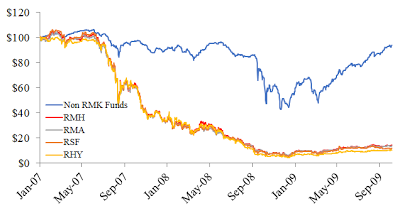

These funds did not behave like their peers. Below is a graph which compares the total returns of the RMK closed-end funds with non-RMK closed-end high income funds from January 2007 to December 2009.

Six of the eight directors sat on the Fund's Audit Committee and were designated as "Audit Committee Financial Expert." Their task was to oversee the process of determining the fair value of the funds. According to the SEC order, the directors did not provide any guidance on how to determine fair value. Many of these securities were in structured finance that were below investment grade. Also, they were highly leveraged and illiquid. Some of the reported values for these illiquid securities went unchanged for several months before the turmoil in the subprime MBS market.

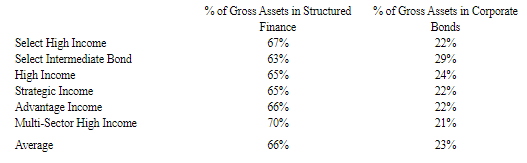

In our 2009 paper, we calculated that about 60% or more of the gross assets of these funds were in structured finance. We also calculated that more than 80% of the losses between March 2007 and December 2007 were in asset backed securities and/or from internally priced securities--the securities that the SEC alleges the eight directors had a responsibility to accurately value.

RMK Funds Were Structured Finance Funds March 31, 2007

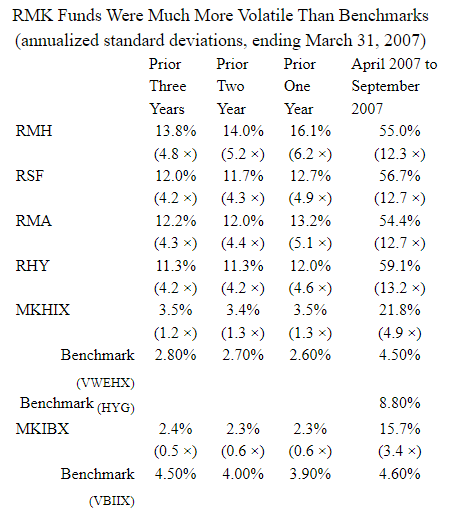

Morgan Keegan also misrepresented some of these asset backed securities as corporate bond or preferred stock. For example, most of all of the securities classified as "Corporate Bonds - Special Purpose Entities" are asset backed securities. Moreover, RMK misrepresented the riskiness of the funds. The RMK funds were four to six times as volatile as their benchmark during the 1-year, 2-year and 3-year periods ending on March 31, 2007. They were more than 12 times as volatile as their benchmark.

RMK Funds Were Much More Volatile Than Benchmarks (annualized standard deviations, ending March 31, 2007)

In June of 2011 the SEC settled with Morgan Keegan & Company and Morgan Asset Management for $200 million and barred former portfolio manager James C. Kelsoe Jr. and suspended comptroller Joseph Thompson Weller.