Structured Products Highlight: JP Morgan Reverse Exchangeable Linked to Ford

Dec 2012

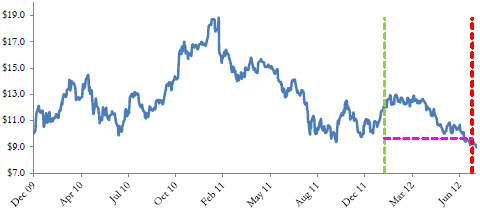

Today we're highlighting a structured product issued on January 19, 2012 by JP Morgan. This product (CUSIP: 48125VHZ6) is a Reverse Exchangeable linked to Ford Motor Company (F). Investors who purchased the notes were exposed to the possibility that JP Morgan would default on the obligations spelled out in the note's offering documents.

This particular note offered investors monthly coupons at an annualized rate of 11.25% for the six month term of the note. If, during the term of the notes, Ford's common stock share price depreciated by more than 20% of the price observed on January 19, 2012 then investors would lose the buffered protection offered by the notes. This trigger event would then result in either 83 shares of Ford being delivered at maturity or the $1,000 face value (whichever is less). If Ford's common stock share price remains above the 80% buffer level described by the notes then the notes return the face value.

At issuance, we valued this particular product at about $0.964 per dollar invested. The difference is partially accounted for by the stated fees; however, the remainder is an indication that investors were either under-compensated for the put option embedded in the notes or should have been compensated by higher coupon payments. During the term of the notes, Ford closed below the buffer level and a trigger event occurred.

At maturity, investors received about 83 shares of Ford common stock (or an equivalent cash amount) per $1,000 invested in the notes. As a result, investors realized a -32% annualized rate of return including the monthly coupon payments made by JP Morgan during the term of the notes.