We've been looking through some historical issuances of structured products recently and we happened to come across a peculiar product issued by Morgan Stanley in September 2008. The product (CUSIP: 617483664) offered investors bearish exposure to the S&P 500. In other words, if the S&P 500 level declines as of the valuation date of the notes, then the product would exhibit a positive return.

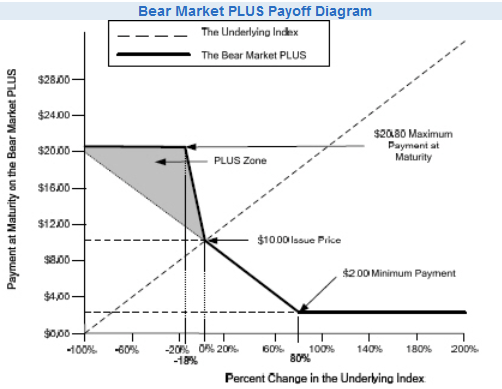

Not only was the return positive if the S&P 500 went down, but it was leveraged six times -- capped at a maximum return of 108%. So if the S&P 500 level declined by 18% or more between the issue date and the valuation date, the investor would have received more than double their initial investment from Morgan Stanley. Here is the payout diagram from Morgan Stanley.

Obviously, this investment would do particularly well if the S&P 500 declines. Amazingly, the pricing date for this product was September 23, 2008: precisely before one of the largest market collapses in history:

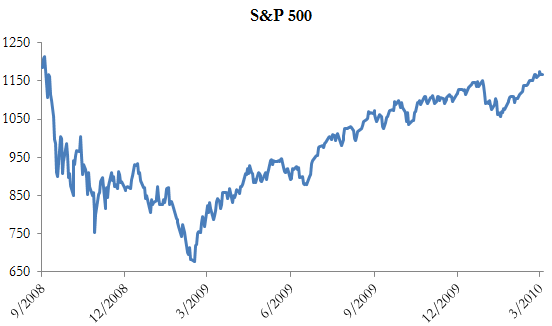

You might think that whoever purchased this product was a genius. Indeed, the timing of this issuance was impeccable; however, the proverbial stick in the mud is the fact that the valuation date wasn't until March 2010. On September 23, 2008, the S&P 500 level was 1,188.22 -- this determines the initial index level. At the close of business on the valuation date (March 26, 2010), the S&P 500 level was 1,166.59. Not much of a loss on the S&P 500, and therefore not a mind-blowing return on this bearish structured product.

Even though the S&P 500 posted a closing level decline of over 40% during the term of the note, the closing level on the valuation date was only 1.8% lower than the initial index level. Investors still earned nearly nearly 11% on their investment--much better than a direct investment in the S&P 500--but nowhere near the maximum return even given the financial crisis.

This product highlights one of the primary difficulties investing in illiquid securities: not only did this structured product investor have to pick the right size and direction of a price difference, but also exactlywhenthat difference would exist. If the maturity date had been a little earlier or even a little later, the investor's return would have been very different, and since there is only limited secondary markets for structured products, he or she could not have sold the product when a similarly structured liquid investment would have been worth much more.