Craig McCann has testified in virtually all of the FINRA arbitrations involving the type of hedge fund mentioned in the Bloomberg and USA Today stories as well as others against Citigroup: Hosier, Puglisi,Barnett, Beard, Berghorst, Abramson, Coleman, Silk, Miller, Selan and Bach. In addition, Craig has testified in cases involving other funds such as First Republic's TW Tax Advantaged, Aravali, 1861 and Stone & Youngberg's Municipal Advantage Fund. We've discussed these funds in previous blog postsand in a working paper.

Marketed as an arbitrage strategy, the MAT/ASTA and other similar funds were simply high-cost, highly-leveraged bets on interest rate, liquidity and credit risk in municipal bonds. Brokerage firms, including Citigroup, misrepresented the strategy by comparing the yields on callable municipal bonds with the yields on non-callable Treasury securities without adjusting the yields on municipal bonds for their embedded call features and by ignoring 30 years of published literature which demonstrates the remaining difference in after-tax yields is compensation for liquidity and credit risk. The losses suffered by investors were suffered during a period of relatively routine interest rates and not during an unprecedented interest rate environment.

Nearly two years ago in a 2010 WSJ story, Dr. McCann was quoted as saying that Citigroup would end up having to pay out tens of millions of dollars to investors in the MAT/ASTA funds. With the $85 million Citigroup has paid so far with no end in sight, the total tally for Citigroup's folly is likely to be much higher. In addition, ongoing regulatory investigations into the sales of the MAT/ASTA funds dogs Citigroup four years after the funds failed.

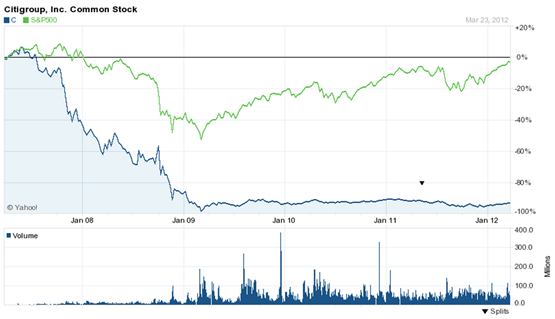

Perhaps far more costly for Citigroup is the harm to its franchise. As this Yahoo Finance graph illustrates, Citigroup's shareholders have suffered terrible losses as the firm provided disservice to its clients.