More Impossible Trade Prices Caused by Auto-liquidators: Option Combinations

Dec 2015

In three previous blog posts, we documented how auto-liquidators execute option trades at distorted prices to their clients' detriment. The price distortions are caused by the price impact of large sell or buy orders on thinly traded securities. These distortions were reversed within minutes, but not before causing investors millions of dollars of unnecessary losses.

In "The Recent Market Turmoil Spells Trouble for Auto-liquidators like Interactive Brokers", we showed that thinly traded long-dated, deep out-of-the money SPX put options were bought on August 24, 2015 at implausibly high prices, purportedly to cure margin deficiencies. We showed the price of one SPX put option increased from $4 to as high as $83 in seconds as a result of auto-liquidation transactions after which the option price quickly dropped back to around $4. These auto-liquidation trades converted an account from a credit balance to a debit balance in seconds when a rational liquidation would have cured the margin deficiency and left the account equity intact.

In "More Signs of Trouble for Auto Liquidators", we explained how rational liquidations would have saved an auto-liquidated account using another stylized example from an account that was liquidated to a debit balance during the morning of August 24, 2015. We used prices of near expiration, at-the-money call options on Barclay's VXX ETN linked to the VIX index with different strikes to demonstrate the harm caused by auto-liquidations that occurred while an investor was blocked from making trades in alternative strike prices within the same options class.

In "Only a Faulty Auto-liquidator Pays More for An Option Than it Can Ever Be Worth" we documented transactions executed by auto-liquidators which no informed, self-interested trader would execute, because the buyers paid more for a security now than it can ever be worth in the future. Our examples in that post were closing trades in short put options in which the buyers paid more than the put options' strike prices. Since the put options' payoffs at maturity will be received in the future and can never be more than the strike price, no one would pay a price greater than or equal to the put options' strike prices.

In this post, we provide additional examples of transactions involving option strategies - combinations of options - at theoretically impossible prices.

Option Strategies

Option investors can trade several different options on the same underlying asset at the same time instead of buying or selling a single put or call option. For example, a calendar spread trade involves selling one option and buying another option on the same underlying asset with the same strike price but with a longer maturity.

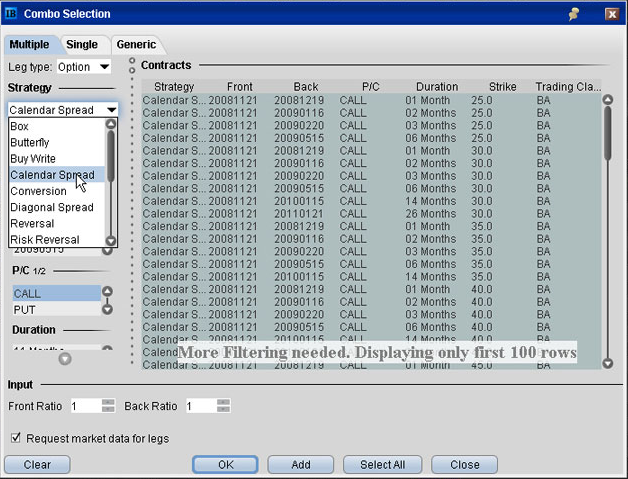

Combining options on the same underlying asset with different maturities or strike prices is a common strategy to get some leveraged, but limited, exposure to the underlying asset's returns. All component options in the option strategy are usually purchased at the same time. In fact, the option trader can submit a single order for certain option combinations specifying the maximum price he is willing to pay for the package and each component is executed simultaneously. There is no need to specify the price for the individual component. For example, Interactive Brokers illustrates how to search a spread strategy and bid the option strategy using its trading software . If the order is marketable, IB will fulfill the order no greater than the spread price specified. The order, which involves purchasing or selling several options is executed at the same time.

Figure 1. Interactive Brokers Spread Order Combo Selection

Bull Call Spreads

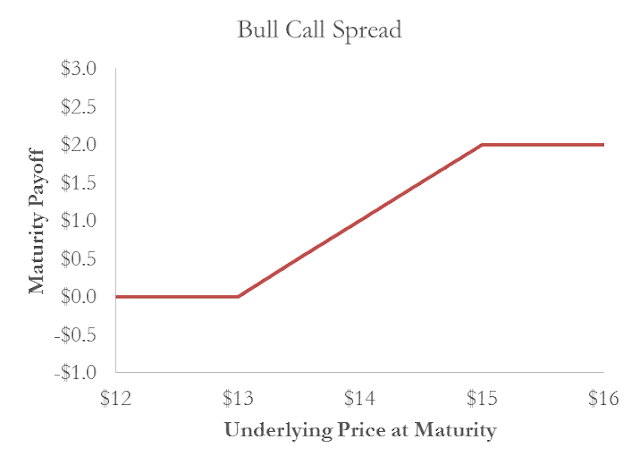

A bull call spread is a standardized option strategy, involving the purchase of a call option and the simultaneous sale of another call option with a higher strike price but otherwise identical. In Figure 2, we draw the final payoff of the bull call spread created by buying a call option with a $13 strike price and selling a call option with a $15 strike price.

At maturity, if the underlying price is below $13 both options expire worthless and the holder of this bull call spread receives nothing. If the underlying price closes between the strike prices, i.e., between $13 and $15 in our example, only the lower strike call option pays off and the holder of the bull call spread receives the amount by which the underlying asset closes above $13. If the underlying asset closes above the higher strike price, the holder receives the excess of the underlying asset's closing price over $13 but gives up the excess of the underlying asset's closing price over $15 - netting exactly $2 in our example.

No investor would ever pay more for a put option than its strike price because that is the most the option will ever be worth. The same logic applies to option combinations like the bull call spread illustrated in Figure 2. Since that option combination can never pay more than $2 - and will often pay less than $2 - no trader will willing pay $2 or more for this option combination.

However, it appears that an auto-liquidator recently executed this option combination trade at theoretically impossible prices. We list simultaneous August 24, 2105 trades in VIX call options expiring on September 16, 2005 in Table 1. A $13 strike price call option was purchased for $15 and, simultaneously, a $15 strike price call option was purchased for $12.4. Somebody paid $2.6 for the call bull spread with a maximum payoff of $2 at maturity. Even though both prices fall within their national best bid and offering ("NBBO"), the price paid for this option combination was theoretically impossible.

Table 1. Bull Call Spread Trade at Theoretically Impossible Prices

Bull Put Spreads

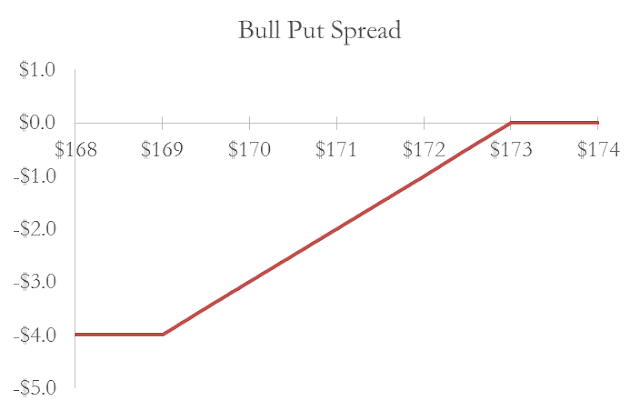

The payoff of the bull put spread is similar to the payoff of the bull call spread. The bull put spread involves selling a put option and buying a put option with a lower strike price. Instead of paying a premium for the bull call spread, the buyer of the bull call spread receives a premium, the difference in the prices of the options that she purchased and sold. The maturity payoff to a bull put spread with $169 and $173 strike prices is plotted in Figure 3.

Figure 3. Payoff of Bull Put Spread

Bull put spreads, like bull call spreads, have higher payoffs when the underlying asset's price is higher, rather than lower, at expiration. An investor with a bull put spread will have to payout between $0 and $4 if the price of the underlying asset closes between $169 and $173 when the option expires. If the underlying asset closes below $169, the investor pays out $4; if the underlying asset closes above $173, the investor pays out nothing.

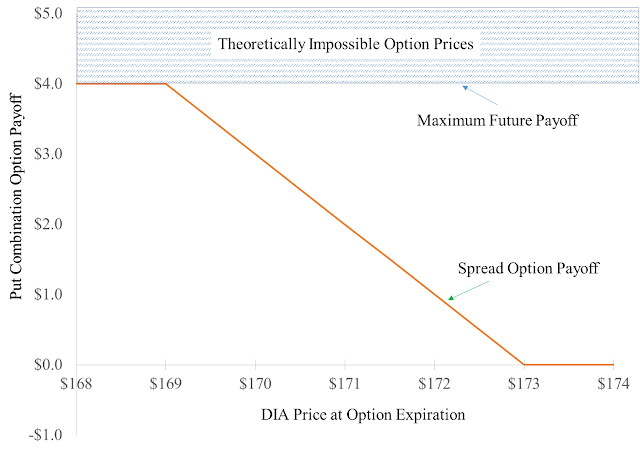

An investor with a bull put spread can close out this position by buying the higher strike price put option and selling the lower strike price put option. The maximum payoff to buying the higher strike price put option and selling the lower strike price put option is the difference in strike prices. The most an informed trader would be willing to pay to close out the bull put spread thus is the difference in strike prices.

Figure 4. Payoff of Closing Bull Put Spread

On August 21, 2015, a bull put spread trade on the SPDR Dow Jones Industrial Average ETF expiring that day was executed at a theoretically impossible price. The options' strike prices were $169 and $173 so the spread's maximum theoretical price was $4 but the spread trade was executed at $4.16 (i.e. $5.90 - $1.74). See Table 2.

Table 2. Put Bull Option Trade at Theoretically Impossible Prices