The securities industry has long targeted the liability side of the customer's balance sheet as an opportunity to cross-sell banking products, increase wallet share, and diversify revenue streams away from cyclical trading commissions. In the current euphoric market environment, with portfolio values soaring and borrowing rates historically low, lending to customers has become "Wall Street's hottest business."i However, the proliferation of these securities-based loans ("SBLs") is cause for serious concern. While securities-based lending is a low-risk and very profitable business for the broker-dealer, the same cannot be said for the borrower. Broker-dealer lending creates serious conflicts of interest, saddling the customer with risks and potential long-term consequences he or she may not fully understand until the next bear market arrives.

Securities-Based Lending

There are two types of SBLs. The more familiar is the margin (or purpose) loan. Margin loans are "credit extended for the purpose of buying, carrying, or trading in securities."ii Securities in the customer's account serve as collateral. Broker-dealers are also permitted to extend credit, generally secured by a customer's marketable securities, for purposes other than buying or carrying securities.iii These loans are known as good faith or non-purpose loans. The real growth in lending has come from non-purpose loans.

Margin loans and non-purpose loans are similar in many ways. The underwriting for either loan gives little or no consideration to the borrower's credit rating, income, or debt ratios. The amount of credit extended primarily is a function of the value of the collateral securities, the liquidity and volatility of those securities, and the extent to which there is any concentration in a single security. Establishing either type of loan involves relatively little documentation compared to other types of lending. Each loan requires a minimum level of equity (loan-to-value) at inception and is subject to calls for additional capital if the value of the collateral falls below a stated minimum. Most SBLs charge variable interest rates at a spread pegged to either 30-day LIBOR (in the case of a non-purpose loan) or the broker call rate (in the case of a margin loan). Neither type of loan requires a fixed repayment schedule. Instead, interest is charged monthly and added to the loan balance.

In spite of these similarities, non-purpose loans are different from margin loans (and other conventional loans) in important ways. The primary difference is that a non-purpose loan may not be used to purchase or carry securities. Instead, these loans are often recommended to finance real estate transactions, buy automobiles or boats, or fund businesses. Brokers also recommend non-purpose loans to pay taxes,iv take a vacation, pay for a wedding, even to replace retirement account withdrawals in years when the equity markets are down.v

SBLs Are Highly Profitable

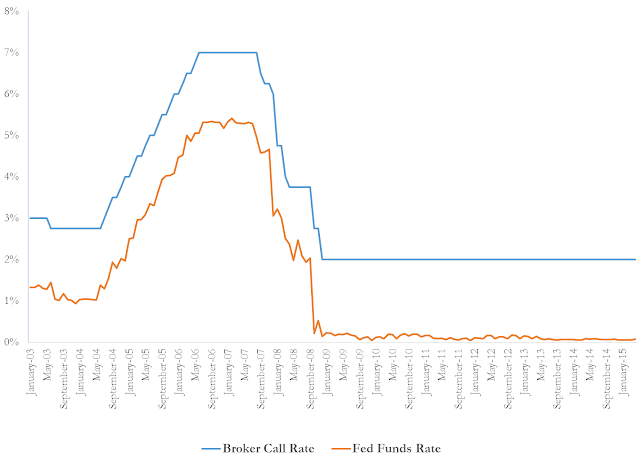

Substantial profit margins in the lending business make SBLs a lucrative product for broker-dealers. Last year alone Morgan Stanley and UBS earned a combined $4 billion in net interest income just by opening their doors for business. Brokers fund much of their operation by borrowing in the overnight repo market,vi where the Federal Funds Rate has been less than 0.15% for the past two years. See Figure 1. The difference between the Broker Call Rate and the Fed Funds Rate averaged 1.66% in 2003 and has grown to 1.93% in 2014 despite the dramatic decline in interest rates. Most loan customers are charged a variable interest rate pegged to a spread over LIBOR, allowing the broker to charge higher rates if its cost of funds increases.vii Spreads between the cost of funds and loan rates generally range from 200 basis points (for loans up to $10 million) to 500 basis points (for smaller loans),viii and the revenue is predictable and recurring.

Figure 1. Broker Call Rate and Fed Funds Rate

To market these loans, broker-dealers use advertising - disguised as client education - that is often misleading, one-sided, and not fairly balanced with disclosure of the risks associated with SBLs.ix UBS, for example, extols the wisdom of "borrowing with a vision for your future",x and "maximizing the power of your invested assets."xi Morgan Stanley portrays borrowing as a way to "unlock the value of [the customer's] portfolio."xii It claims that borrowing "puts the value of [the customer's] assets to work."xiii Merrill Lynch tells clients that borrowing money will "keep [their] investment strategy on track."xiv After reading these characterizations of borrowing, a customer cannot not be blamed for concluding that he is imprudent if he is not borrowing against his portfolio.

Since adviser behavior is driven by personal financial considerations, broker-dealers offer meaningful incentives to their brokers for recommending SBLs. Morgan Stanley's compensation plan is typical. The broker earns an annual gross commission of 0.40% to 0.50% of his clients' loan balances outstanding. Morgan Stanley also pays its Financial Advisors based on growth in the volume of loans made to clients. For example, a broker who recommends $25 million in new loans is paid a cash bonus (deferred for only five years) of over $100,000. At UBS brokers are also paid based on the total value of the loans their clients have taken on. UBS even rewards secretaries suggesting SBLs as an alternative to customers who are calling to withdraw money from their accounts.

Suitability

The suitability principle applies both to individual transactions and overall investment strategies.xv It requires that any recommendation, including the recommendation of an SBL,xvi be consistent with the interests of the customer.xvii Even if a customer wishes to take out an SBL, the broker may not make that recommendation if the loan would not be suitable. SBLs must be considered part of an investment strategy and subject to FINRA Rules 2090 and 2111. Investing with borrowed funds only makes sense if the expected returns net of the borrowing costs are sufficient to warrant the risks of the additional investments. For low risk, low return investments, SBLs give investors certain but negative returns. For higher risk, higher return investments, SBLs give investors small positive expected returns but expose them to substantial losses.

Central to the overwhelming case for diversification is the observation that competition among investors bids up the prices of securities so that the expected returns to portfolios of stocks and bonds exceed the risk free rate of interest by just enough to compensate for the risks of those portfolios. The expected return to making additional investments on margin, for investors who pay more than the risk free rate to buy securities, is therefore less than what the market requires for bearing those risks. For example, with risk free rates around 2% and the equity risk premium about 6%, if an investor borrows at 5% the expected net return is only 3% (2% + 6% - 5%) for bearing risk investors in the aggregate demand 6% net returns.

Leverage and borrowing costs are not the only suitability considerations associated with SBLs. Unlike home mortgages or car loans, which require the borrower to make a monthly payment, most SBLs simply add each month's interest charge to the loan balance, thus compounding the interest expense.xviii In addition to the financial risks, SBL borrowers have no protection from actions taken by broker-dealers to preserve their collateral. Loan accounts are susceptible to forced liquidation at unfavorable prices because, as the value of the securities declines, the borrower must either deposit additional collateral (which he often does not have) or sell multiples of the amount of his margin call.xix Furthermore, the broker can effect these sales without contacting or seeking the permission of the borrower.xx The broker can even choose unilaterally which securities it wishes to sell. A customer with no means of meeting margin calls other than by selling the collateral is generally not suitable for an SBL.

When recommending an SBL, the broker must consider virtually all aspects of the clients financial condition: income, which would determine ability to service the debt; other assets, liquid and illiquid; other debt outstanding; and the client's ability (and willingness) to tolerate the risks of an SBL.

Several questions should be considered before a broker-dealer recommends an SBL: • How much debt (from all sources) does the client currently carry? • Will this loan create more debt than is justified by the client's financial circumstances? • What are the client's liquid assets, apart from the collateral securities? Does the client have sufficient liquidity to meet margin calls? • Is the additional risk created by the financial leverage suitable for the client? • Does the client understand all the risks of an SBL? • To what purpose is the loan being applied? Will the client have a means of repaying the loan? • Are asset sales a better alternative?

Non-purpose loans, by definition, are not invested in liquid securities. In fact, many non-purpose loans are not used to purchase assets of any kind; the funds are simply consumed by taxes, vacation costs, or similar consumption expenditures. This situation raises a major red flag for the recommending broker because it suggests the customer does not have the capacity to meet margin calls other than by liquidating the collateral securities. In those circumstances the broker would have a difficult time justifying as suitable the recommendation of a non-purpose loan because the borrower's "financial ability to meet such a commitment"xxi is in doubt.

Conclusion

Securities-based lending presents some of the most serious conflicts of interest in the broker/client relationship. It puts brokers and RIAs, who are supposed to be investment professionals, in the position of recommending an action that often is detrimental to their clients' long-term goals of wealth preservation and capital growth. Almost two-thirds of American households headed by someone age 55 or older are already in debt.xxii Debt is a drag on net worth and a lien on future income. Debt inhibits the client's ability to accumulate retirement savings. Reducing debt, on the other hand, increases net worth and improves cash flow.

Each bull market develops its own excesses, thus planting the seeds for the next correction. Investors with already illiquid balance sheets are flocking to SBLs today in unprecedented numbers, due in no small part to the aggressive marketing of SBLs and the attractive financial incentives offered to brokers who recommend them. One way or another, however, these loans will eventually come due. For too many borrowers that due date will come near the bottom of the next bear market. These customers will be the last ones out, and the effects will be financially devastating.

_______________________________________

i Joshua Brown, The Rise of Rich Man's Subprime, Fortune.com, December 10, 2014. ii Regulation T, §220.2. iiiSee, FINRA Rule 4210(e)(7), "In a nonsecurities credit account, a member may extend and maintain nonpurpose credit to or for any customer without collateral or on any collateral whatever;" "The term 'nonpurpose credit' means an extension of credit other than 'purpose credit' as defined in Section 220.2 of Regulation T;" see also, Regulation T, §220.6. ivSee for example Morgan Stanley, Tax Payment Strategies: Portfolio Loan Account. vSee Investment News, The hazards of securities-based lending as a source of retirement income,February 11, 2015, Michael Crook, head of portfolio planning and research, UBS, says an SBL can be used in lieu of cash withdrawals as a source of retirement income. vi Eric S. Rosengren, President & Chief Executive Officer, Federal Reserve Bank of Boston, Keynote Remarks: Conference on the Risks of Wholesale Funding, sponsored by the Federal Reserve Banks of Boston and New York (August 13, 2014), "Short-term collateralized loans called repurchase agreements are a major source of funding for [broker-dealers]." viiPutting Stocks in Hock: Securities Are Backing for More Big Loans, Wall Street Journal, March 4, 2013, "Non-purpose loans, by contrast, can typically be completed in a few days requiring little paperwork beyond a credit report and a financial statement." "Another big benefit: For wealthier investors, interest rates on non-purpose loans can be attractive compared with alternatives. At UBS, for instance, investors borrowing between $1 million and $2.5 million pay 2.95% based on the latest London interbank offered rate. By contrast, the national average rate for a home-equity line of credit is 5.15% and for a 30-year "private" jumbo mortgage it is 4.08%, according to HSH.com, which tracks the data." viii James P. Gorman, Chairman and Chief Executive Officer, Morgan Stanley, Strategic Update, January 20, 2015, Morgan Stanley currently enjoys a 280 basis point spread between its cost of funds and its interest income. They believe that spread will increase to almost 400 basis points in 2015. ixSee generally FINRA Rule 2210(d)(1)(A), Communications with the Public, Content Standards, "All member communications with the public shall be based on principles of fair dealing and good faith, must be fair and balanced, and must provide a sound basis for evaluating the facts in regard to any particular security or type of security, industry, or service. No member may omit any material fact or qualification if the omission, in the light of the context of the material presented, would cause the communications to be misleading;" see also, Morgan Stanley publishes a 1600-word brochure, Securities-Based Lending: Portfolio Loan Account, that devotes only eight words to the risk of leverage in a portfolio: "market conditions can magnify any potential for loss;" see also, FINRA Regulatory and Examinations Priorities Letter (2015), FINRA "is concerned about how [SBLs] are marketed." xhttps://onlineservices.ubs.com/OLS/jsp/HomePage.jsp, January 13, 2015. xiIbid. xiiMorgan Stanley, Securities-Based Lending: Portfolio Loan Account. xiiiIbid. xiv Merrill Lynch, LMA account. xv The concept of investment strategy "is to be interpreted broadly," FINRA Rule 2111, Supplementary Material. xvi Office of the Comptroller of the Currency, Comptroller's Handbook, Retail Non-deposit Investment Products, January 2015, "Margin credit, however, is not suitable for all clients due to the associated risks and requirements with having margin in an account." xvii See, for example, FINRA 2015 Regulatory and Exam Priorities Letter, "A central failing FINRA has observed is firms not putting customers' interests first. This principle should be observed whether the firm "must meet a suitability or fiduciary standard." xviii Merrill Lynch calls this feature "flexible repayment options," Merrill Lynch, Loan Management Account. xixSee FINRA, Investing with Borrowed Funds: No "Margin" for Error, "Investors who cannot satisfy margin calls can have large portions of their accounts liquidated under unfavorable market conditions. These liquidations can create substantial losses for investors." xxSee generally FINRA Margin Disclosure Statement. xxi Rule 2111.06. xxii Craig Copeland, Ph.D., Debt of the Elderly and Near Elderly, 1992-2013, Employee Benefit Research Institute.