Structured Products Highlight: UBS Autocallable Linked to JOY

Nov 2012

Today we're highlighting a structured product issued on July 25, 2012 by UBS. This product (CUSIP: 90269T574) is a Trigger Phoenix Autocallable Optimization Security linked to Joy Global Inc. (JOY). Since this product is issued by UBS, purchasers of the notes were exposed to the possibility that UBS would have been unable to meet the obligations spelled out in the note's offering documents.

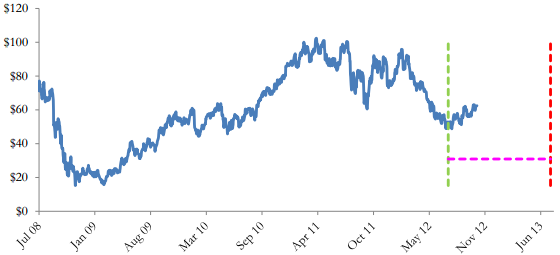

This particular note offered investors quarterly coupons (annualized rate of 12.84%) if JOY's stock price is above the coupon barrier -- $30.92, or 60% of the July 20, 2012 closing price of JOY -- on the quarterly coupon dates. This product has an embedded call feature that is automatically triggered if JOY's stock price exceeds the July 20, 2012 value on any quarterly coupon date. If the product is not called prior to maturity (July 22, 2013), investors receive their principal investment unless JOY's stock price is below the coupon barrier. If the stock price is below the coupon barrier at maturity and the product has not been called, investors lose a percent of principal for each percent decline of JOY's stock price over the term of the note.

This particular autocallable recently had its first coupon date on October 22, 2012 and because JOY's stock price at the close of business on October 22, 2012 was above that value on the pricing date, the product was called. Investors received their principal as well as the quarterly coupon due ($0.3210 per $10 of principal). The following figure graphically depicts JOY's stock price and shows that the price increased during the first quarter of the note's term.

At issuance, we valued this particular product at about $0.97 per dollar invested. The difference is partially accounted for by the underwriting discount; however, the remainder is an indication that investors should have been compensated by a higher coupon rate on the notes by UBS.