Structured Products Highlight: Reverse Exchangeable Linked to Apple

Nov 2012

We here at SLCG have been working on research reports to educate investors concerning recent offerings of structured products. We've talked a lot about structured products on this blog and we wanted to start describing the features of individual products and how we analyze their value.

Today we're highlighting a structured product issued in August 2012 by JP Morgan. This product (CUSIP: 48125V4K3) is a Reverse Exchangeable Note linked to Apple stock (AAPL). Reverse exchangeables -- also known as reverse convertibles -- generically pay periodic coupons. If the underlying asset does not close below the product's trigger price throughout the term, the product returns principal. If the underlying asset does close below the trigger price at some point during the term and the closing price on the maturity date is below the initial price, the notes are converted into a specified number of shares and/or cash at maturity. Since this product is issued by JP Morgan, purchasers of the note are exposed to the possibility that JP Morgan will be unable to meet the obligations spelled out in the note's offering documents.

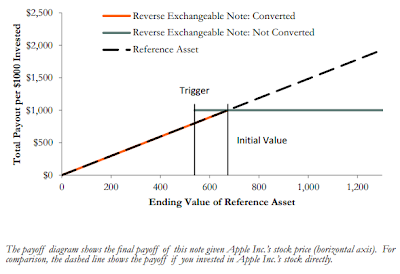

This particular reverse exchangeable had an offering size of nearly $2 million, pays monthly coupons at an annualized rate of 9.25% and matures on August 30, 2013. The trigger price was set to $538.90 (80% of the trade date price). If a trigger event has occurred (AAPL closed below $538.90 between August 31, 2012 and August 28, 2013) and AAPL's price on August 28, 2013 is below $673.63, then the note will convert to 1.48 shares of AAPL stock. The following figure illustrates the payoff at maturity for these notes.

At issuance, we believe the product's fair value was roughly $0.955 per dollar invested based upon the decomposition we used. The difference between this fair value and the purchase price is the compensation JP Morgan receives for offering the notes (4.5%). Since this amount is beyond the 3.5% of fees and commissions collect on the notes, JP Morgan has not offered a sufficiently high coupon to compensate investors for the put option they have sold JP Morgan on the issue date.

Just last week -- on November 8, 2012 -- AAPL closed below $538.90 for the first time since the August 31, 2012 and so a trigger event has occurred. As a result, if AAPL closes below $673.63 on August 28, 2013, the notes will be converted into 1.48 shares of AAPL stock.